Disclaimer: To avoid any confusion, the term rent in the title refers to economic rent, the returns to finite assets. It does not mean the contract rent gotten from leasing out any asset to another person.

When it comes to the market economy, there exists a fundamental distinction between the goods and services, be it as laborers or as investors in capital, which people make, and the finite assets, most especially land, which people take. The free market is predicated on the idea that any increase in demand and the price paid for a good or a service should be matched by an increase in the supply of that good or service, both to reduce prices and make said good or service more abundant. Pursuant to this idea is the belief that new competition should be able to come in to a specific market and reduce the power of incumbent producers, preventing them from accumulating wealth while not meeting the demands of society.

But this core idea drives itself into a ditch when it comes to those things which are finite, things which humans can not produce more of regardless of how scarce and sorely needed they become, and the unearned income they bring in to their owners. The early thinkers of free market-oriented Liberalism like Adam Smith recognized this core principle as far back as the late 18th century, yet instead of heeding their warnings we have instead been treating the finite things of value in this world as a core economic investment. The result has been a myriad of economic failures, extremely unequal outcomes, and an outright misuse and abuse of nature’s bounty, all because we forgot this fundamental distinction in our market economy.

Economic Rent Comes in Many Forms

Before we cover how dealing with economic rents can reconcile equity and efficiency, we first need to cover the various forms in which it comes. There are various sources, so to simplify here is a bulleted list of them listed under special categories (taken from these sources: Peter Smith Rewilding and Liberal Currents):

- Natural resources:

- Land

- Subsoil resource deposits (e.g. minerals and oil)

- Water rights

- The electromagnetic spectrum

- Orbital slots in space

- Timber rights on forested land

- Fishing rights

- Rights-of-way (more on this in the natural monopolies section)

- Legal privileges:

- Patents (medicines, software, industrial designs)

- Copyrights (software, like DMCA section 1201, and broader media)

- Limited occupational licenses, especially when reinforced by associated professional organizations (e.g. medical licenses and the AMA)

- Limited government franchise rights (e.g. taxi medallions)

- Natural monopolies:

- Utilities (e.g. electricity, water, and gas services, which all rely on aforementioned rights-of-way)

- Transportation networks like rail (which again rely on rights-of-way to build lines)

- More recently, network effects in data-oriented platforms, which allows those who harness it to constantly accumulate and strengthen their market power and value as their user base grows. Being involved in the world of technology, these network effect moats are also protected and widened by patents and copyrights.

- Finally, outright monopolies-of-scale, as described by Henry George himself

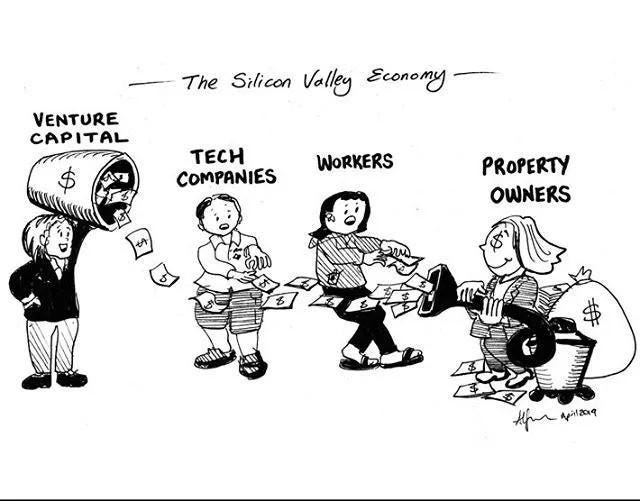

By having the special power of being able to control these finite assets, be it a particular plot of land or the privilege of being at the top of a naturally monopolistic industry, owners can charge extra out of society without needing to fear new competitors coming in to undercut them. Nobody can fold the Earth over itself to make a second Manhattan or any more beyond it, which is why Manhattan land in 2014 was worth about the same as all of Canada’s GDP in 2014. Granted, Manhattan is one of the great economic hubs of the World; but still that value which accrues to landowners, who do not need to do any work and investment to capture the economic rent of land, is value wasted in paying for a resource whose supply we can’t increase.

Market Failure

It’s here where the economic struggles begin with putting our economic eggs into the basket of finite assets, and land serves as the perfect example. As land in a particular location grows more valuable with the growth of the community and investment around it, so too does the incentive to buy it, sit on it, and wait for its price to rise. This practice, called land speculation, only worsens the issue as, instead of using our most necessary finite resource efficiently and wisely, speculators instead hold land bare while actual prospective users are forced to worse parcels with fewer prospects. Add too the loss of parcels on the market and the increase in the scarcity and price of land, all self-inflicted by our poor public policies, and the cost of land crushes the laborers and productive (not extractive) investors who actually keep the economy afloat.

This also begs the question, to what extent do non-land sources of economic rent drive up the cost of production in the same way land does? How much in the realm of making and giving for each other’s benefit do we lose because restricted medical licenses drive up the scarcity of doctors and healthcare, or because speculators hold out oil deposits and make us use more nature for less return, or because natural monopolies can exercise their inherently unbreakable market power against the people and businesses who rely on them? The social and economic cost of rent-seeking in finite privileges that no new market entrant can compete with is enormous, and land is at the center of it all. This is perhaps best emphasized in the article “Henry George, land speculation, and economic growth and transformation” by Joseph Stiglitz and Tomohiro Hirano:

What is clear, however, is that land speculation (or speculation on any non-produced asset) will detract from productive investment, and that that in turn will have an impact on growth. Policy can mitigate these effects, but financial and monetary policies, designed to stabilize the economy and enhance growth, that do not take into account impacts on the extent of land speculation, may well go awry.

…

But it is not only land rents that divert savings from productive investments that might both deepen capital and facilitate growth-enhancing structural transformation—the capitalized value of monopoly and oligopoly rents may have similar effects. Thus, economic policies that curb rents, in all forms, may be one of the most important tools for promoting the accumulation of productive capital, structural transformation, and economic growth.

Treating finite assets as an investment, resources and privileges all, is a direct wealth transfer from productive workers and businesses to extractive owners, especially our most monopolistic/oligopolistic corporate giants. We can not call a market free while it still falls victim to the effects of monopoly, which are backed by extracting unearned income in those things we can not produce more of.

The Haves vs. The Have-Nots

This element of monopoly, of appropriation and spoilation will, when we come to analyze them, be found largely to account for all great fortunes…

- Henry George, Social Problems, 1883 (link to excerpt)

The privilege of being able to own a thing nobody can reproduce doesn’t just allow extraction without giving anything in return, it also allows those who have finite privileges to directly enrich themselves off making those who rely on their privilege poorer. As the price of land grows in our most valuable urban cities, the price the landless must pay rises too, and so the landowner can accumulate and collect more wealth by requiring a heavier price out of the landless. An example of this two-tier society can be seen in the fact that, on average, landed homeowners have a net worth 43 times that of landless renters. While housing consists of producible housing alongside finite land, the effect of land’s limited nature as a source of the housing crisis can not be understated. This is also before accounting for large-scale landowners and real estate companies that own vast swathes of parcels, be they rural, suburban, or urban.

The problem only gets more extreme when we add on other finite assets too. Assets like mineral deposits, pharmaceutical patents, software copyrights, or a naturally monopolistic business only widen the divide between persons and businesses who own (or have a stake) in their control and those who have to pay the toll they create. Alongside this is the growth in market power a business grants itself being able to insulate from competitors, as well as the problem that our financial system and its assets are heavily tied in to the growth in the value of the finite, especially land; a situation author Mike Bird refers to as The Land Trap.

Of course, this isn’t to say that the only way to get rich is by owning a finite asset, actual productive investment can lead to a vast sum of wealth as well, but it is almost certain that a great deal of our current economic inequality can be pointed back to them. While there isn’t a comprehensive modern study on the effects of all private rents from finite assets on inequality, there is historical evidence that it plays an incredibly important role in explaining inequality. In 1893, at the height of the original Georgist movement’s popularity, Georgist economist John R. Commons wrote the following in an excerpt from his book, The Distribution of Wealth (modified for better reading):

The prime importance of monopoly privileges in the distribution of wealth is well shown by the results of the investigation of the New York Tribune in its efforts to ascertain the sources of the fortunes of the millionnaires [sic] of the United States. That investigation was undertaken to show that the system of protection has not been the main cause for monopolies and great fortunes. The investigation amply demonstrates this proposition. Of the 4047 millionnaires reported, only 1125, or 28%, obtained their fortunes in protected industries. The following partly estimated summaries are given, based on the Tribune report. They show that about 78% of the fortunes were derived from permanent monopoly privileges, and only 21.4% from competitive industries unaided by natural and artificial monopolies. Yet there can be no question that if this 21.4 % were fully analysed, it would appear that they were not due solely to personal abilities unaided by these permanent monopoly privileges. They were mostly obtained from manufactures, and five sixths of the manufactures of the country are based on patents. Besides, fortunate investments in real estate, stocks, etc., have often contributed to fortunes where they do not appear prominently.

Commons’ last line specifically ties back into the question of how hidden finite assets are among broader financial investments. Real estate does involve produced buildings but also hides the effect of finite land, stocks as representations of value can point to produced capital, but can also point to finite assets too. Finding that distinction between production and finitude within these instruments for investment is a topic that needs more care and attention.

Reconciliation

Our current system of taxation fails to make the distinction between that which people produce and that which is finite since reproduction is impossible. Income taxes, sales taxes, the building portion of property taxes (not that which falls on the land), and many of the other taxes we levy all fall on production, directly discouraging it. Worse yet, some of these taxes raise inequality while hampering the productive economy, a double poison.

Meanwhile, the economic rents which accumulate to finite assets are allowed to go to private owners mostly unchecked by the public. There are some locations which do a better job collecting their land values (e.g. Singapore’s methods of land value capture and the split-rate property tax cities of Pennsylvania), but in most locations the return of the value of the finite to the public is little to none.

A recent topic of discussion in economic circles has been the viability of a constant wealth tax above a certain cap as a way to reduce inequality. But similar to the current taxes mentioned in the previous section, a common criticism has been that taxing all wealth can discourage production by targeting the net worth of those who invest in actual productive capital, lowering its supply. It’s a continuation of the fear that there’s a tradeoff between growth and equity.

But what this exercise in understanding private economic rents in finite assets shows us is that we don’t have to trade off growth for equity or vice versa. Private wealth extraction in finite assets already is that feared double poison of inefficiency and inequity seeping throughout our economy. But while this poison may be a killer when left unchecked, it also gives us an obvious antidote, one which can return us that efficiency and equity we’ve long desired. It can perhaps be summarized in a single line:

Don’t tax the value of the goods and services people make, return (or dismantle) the value of the finite assets people take

It is simple, and it likely isn’t the end-all be-all to all economic problems, but it is the best platform to begin building our economy towards being its absolute best.

Leave a comment